“The important thing is the path, not the goal. It is not just about achieving something.”

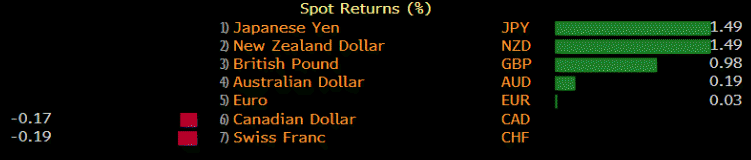

Although the EUR longs remain high at 179K, the net speculative position decreased by 19K.

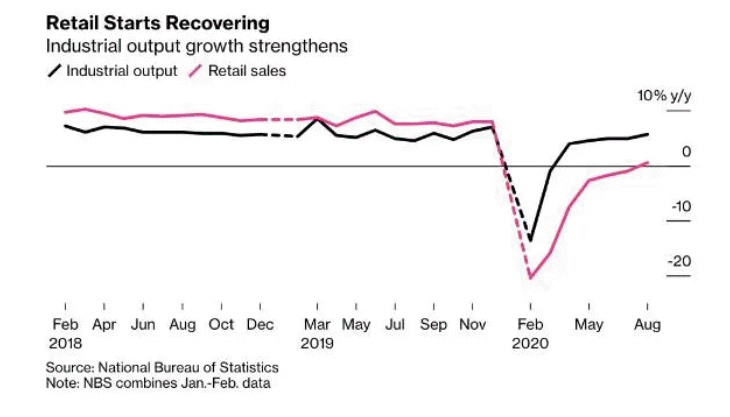

China’s “recovery”, in other words, is largely an exacerbation of the problems that have long been recognised by Beijing. It is a supply-side recovery in an economy that urgently needs more domestic demand but that has found it politically very hard to manage the wealth transfers that it requires.

This recovery isn’t sustainable without a substantial transformation of the economy, and unless Beijing moves quickly to redistribute domestic income, it will require either slower growth abroad or an eventual reversal of domestic growth once Chinese debt can no longer rise fast enough to hide the domestic demand problem

The major US indices are closing the red. The S&P and NASDAQ are down for the 2nd straight day and for the 3rd week in a row. All 11 sectors of the S&P closed lower. The S&P was the weakest of the majors.

For the week, each of the major indices close lower: