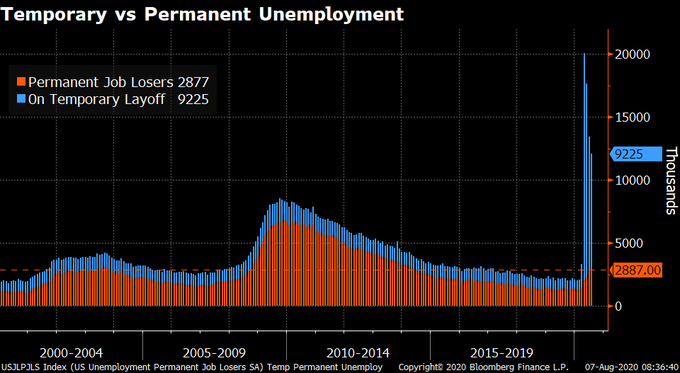

Temporary vs Permanent Unemployment:

“You should have seen the vehemence: No!”“You should have seen their faces: ‘Absolutely not!'”

Government employment rose by 301,000 in July but is 1.1 million below its February level. Typically, public-sector education employment declines in July (before seasonal adjustment). However, employment declines occurred earlier than usual this year due to the pandemic, resulting in unusually large July increases in local government education (+215,000) and state government education (+30,000) after seasonal adjustment.

Swiss foreign reserves declined a little last month but are keeping at rather bloated levels still. In terms of SNB intervention, the weekly sight deposits data offers a better sense of the situation and it still reaffirms that Jordan & co. is actively stepping into the market.