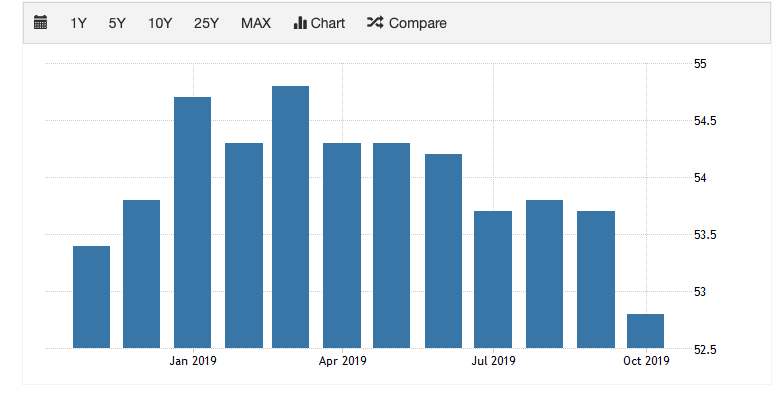

Latest data released by Markit – 2 December 2019

The preliminary report can be found here. A more positive revision here as preempted by the French and German readings earlier but overall factory conditions are still more subdued despite the bit-part recovery.

It just reaffirms that the manufacturing sector is contracting at a slower pace but challenges still remain as we look towards next year.

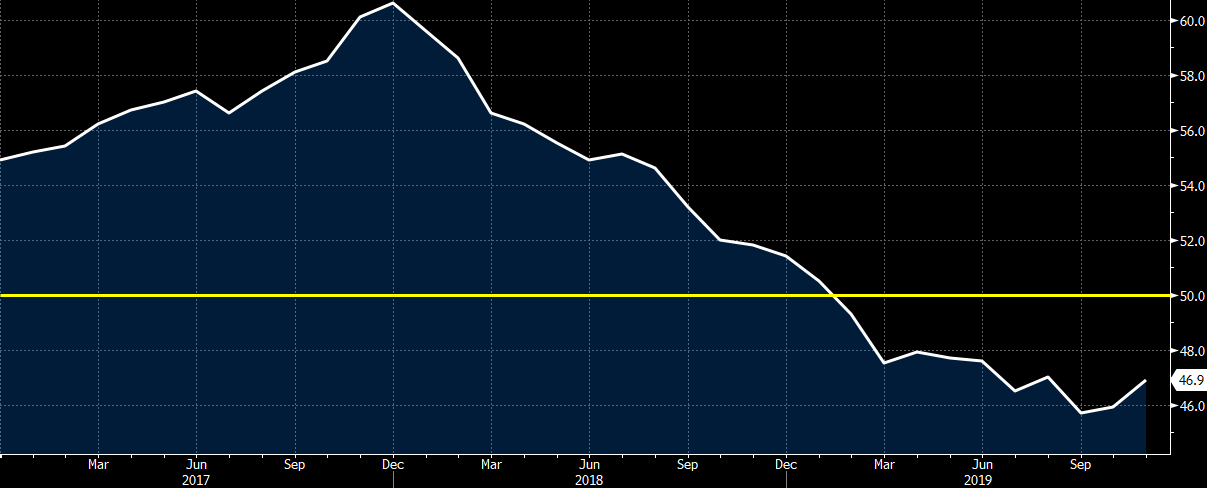

The Caixin manufacturing data has shown a pick up in the last couple of months. October saw a beat of 51.7 vs 51.0 expected with both output and new orders expanding at steeper rates. The official manufacturing PMI release showed an expansion for the first time in 8 months at 51.8 vs 51.5.

The Caixin manufacturing data has shown a pick up in the last couple of months. October saw a beat of 51.7 vs 51.0 expected with both output and new orders expanding at steeper rates. The official manufacturing PMI release showed an expansion for the first time in 8 months at 51.8 vs 51.5.