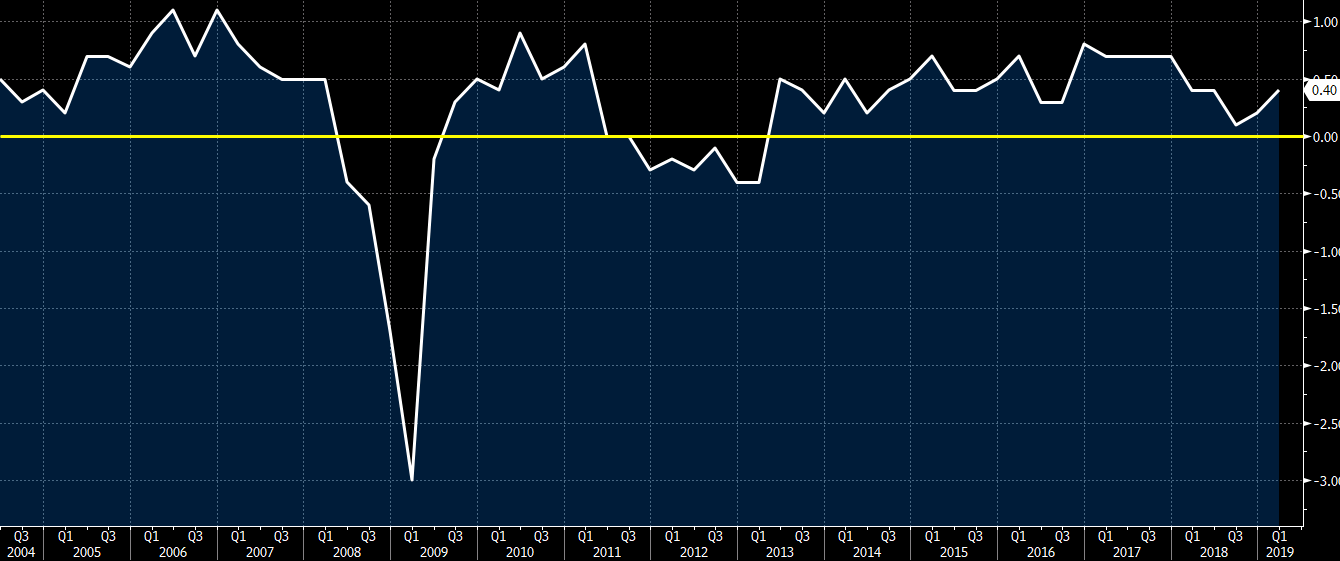

Central Bank Balance sheets v stock market.

Emperor Akihito has abdicated, stepping down from his role as symbol of the Japanese state and becoming the first to voluntarily depart the Chrysanthemum throne in around 200 years.

In a formal, sombre ceremony that began at 5pm local time and lasted around 12 minutes, Akihito read a message of thanks to and offered a prayer that the new era, which begins at midnight and will be called “Reiwa”, would be a stable and fruitful one.

The ritual, which took place in a chamber within the Imperial palace known as the “Room of Pine”, was carried out in front of regalia that include an ancient sword and a sacred jewel.

The abdication was carried out a day ahead of the enthronement on Wednesday of Akihito’s eldest son, Crown Prince Naruhito.

“Since ascending the throne 30 years ago I have performed my duties as Emperor with a deep sense of trust in and respect for the people and I consider myself most fortunate to have been able to do so. I sincerely thank the people who accepted and supported me in my role as the symbol of the state,” said the 85-year old in his final speech as Emperor.

The Emperor’s message followed a short address by the Prime Minister, Shinzo Abe, who thanked him for fulfilling his responsibilities and for giving the Japanese people “courage and hope”.

BP joined its rivals in reporting lower first-quarter earnings compared with a year ago as the UK-listed energy major noted weaker prices and refinery margins.

Underlying replacement cost profits, BP’s definition of net income and the measure tracked most closely by analysts, was $2.4bn in the three months to March 31. This compares with $2.6bn in the same period the year before and analysts’ consensus estimates of $2.3bn.

Chief executive Bob Dudley said in a statement: “We produced resilient earnings and cash flow through a volatile period that began with weak market conditions.”

Oil and gas production from BP’s operations rose 2 per cent from a year ago to 3.8m barrels of oil equivalent per day. This took into account new production from the acquisition of BHP’s US shale assets and projects in Trinidad, Egypt and the Gulf of Mexico coming online in 2019.

Still, higher output was offset by lower oil prices, maintenance activity in the Gulf of Mexico and weather disruptions elsewhere in the US.

Meanwhile, lower refining margins were only partially offset by strong marketing and the overall trading business. Downstream results were hit by “lower industry refining margins and narrower North American heavy crude oil discounts”, BP said. (more…)

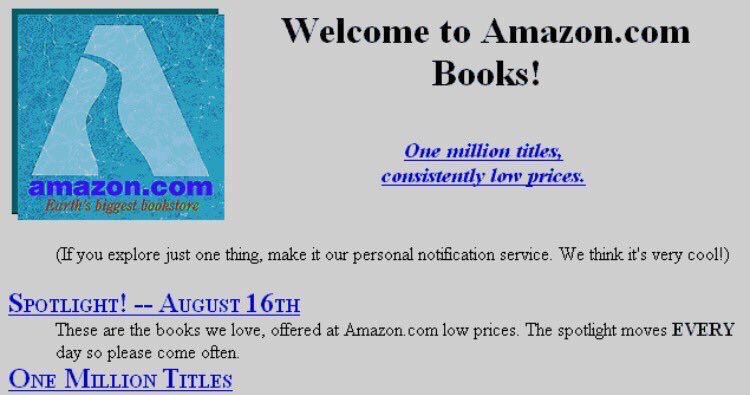

Facebook (2004), Netflix (1999), Amazon (1995), & Google (1997):

Preview here:

Otherwise, from the top:

2200 GMT New Zealand financial statements for 9 months into the fiscal year-on-yearThis is where 2301 GMT UK data – GFK Consumer Confidence for April, expected -13, prior -13

2301 GMT UK data again, Lloyds Business Barometer for April, prior 10

2330 GMT Australia ANZ/Roy Morgan Consumer Confidence, week ended April 28.

0100 GMT New Zealand, ANZ business survey for April

0100 GMT China PMIs, preview here (ICYMI!):

0130 GMT Australia Private Sector Credit for March

0145 GMT back to China for more PMI – this time the Caixin China General Manufacturing PMI